Jump to sections:

- Unleashing the power of data

- South African players ready to drive this revolution

- The fears & challenges of Open Banking

- How does Open Banking benefit banks?

- Open Banking Case Studies

- Does Open Banking augment or challenge how banks make their money?

- What is the way forward for open banking?

South African banks have often been hesitant to embrace open banking technology. As custodians of our money and data, both security and data privacy are understandably top priorities for banks. They hold our value and our transaction history. The depositors they sit on, and the data insights generated drive value for shareholders and sometimes their users. It is for this reason that banks worry open banking may disrupt their traditional business models and give an advantage to newer competitors.

While more banks are joining the conversation around open banking, these concerns remain valid. However, there is potential for new market opportunities if trust and outside partnerships can be established. Open banking requires stringent security measures to protect customer data; therefore, banks must ensure this is considered before implementation. Moreover, it could forge partnerships that could help banks capitalise on fresh sources of revenue while safeguarding their interests at the same time.

A great example of this is how fintechs and banks are both actively modernizing payment methods to drive growth in the economy. To achieve this goal, they are investing in robust banking systems and technology while implementing new regulations related to open banking. This is intended to benefit both banks, by enhancing their value proposition, and third-party providers that will now be able to participate in the payments space on more equal terms. This is just one example of many fintech offerings being rolled out in the open banking environment.

Market projections anticipate that open banking will by 2031, bringing the total market value to more than $123.7 billion. Additionally, global card payments, are set for 9.16% CAGR for the same forecasted period, bringing the total market value to $327.68 billion. If South African banks want to stay ahead, embracing open banking is crucial as global trends forecast significant growth in this ecosystem. It presents a unique opportunity to innovate, cater to customer demands, and secure a competitive edge in the evolving financial landscape.

Unleashing the Power of Data

The Rise of Open Banking

An Open Banking ecosystem is one where a financial institution offers third party providers the ability to connect into the bank’s infrastructure. A common method and one you will hear in the narrative frequently are the use of APIs. Opening up the infrastructure also offers financial institutions the ability to leverage the third party’s technologies to improve their own infrastructure. It is a collaboration outlook and infrastructure that allows all parties to build solutions by plugging in specialised tools for each part of the journey.

It’s clear that the financial ecosystem has changed immensely over the past decade. By no means a new concept, the root of this ecosystem stems from Germany in the 1980s when the German Federal Post Office set up an experiment to test their new online banking service with over 2000 users, and it proved to be incredibly successful as the first self-servicing banking service. This ecosystem further gained traction in Europe with the emergence of the first Payments Services Directive — PSD1 in 2007. The goal of this project was to promote fair competitive practices in the financial sector, resulting in better services for customers and protection for consumers.

Today cash and cheques, physical or card, have lost market share to alternative payment solutions, such as digital wallets, bank-to-bank payments, BNPLs, and cryptocurrencies. According to Boston Consulting Group, 89% of South Africans are turning exclusively to digital banking; this indicates a wider trend in the industry. Meaning an ever-decreasing need for brick-and-mortar facilities to service customers. Open banking is also helping to facilitate financial inclusion for those on the margins of society. Clearly, new payment solutions are here to stay – meaning it’s critical for banks, lenders, and Fintech companies to understand their role in its adoption. A critical example of the success Open banking can drive.

Open banking involves the use of open APIs by third-party providers, granting them secure access to customers’ financial information. This opens opportunities for all key players to leverage innovative technologies and offer services that improve customer experience. Screen scraping and open APIs can permit open banking; however, it’s the latter that is most popular with regulators and banks due to its added security measures. The Euro Banking Association explains that open banking is another mechanism to “bridge worlds” through combining functionalities from banks and non-banks alike. It allows for real-time payments, greater financial transparency options for account holders, as well as marketing and cross-selling options for financial institutions.

A Global Perspective on Open Banking

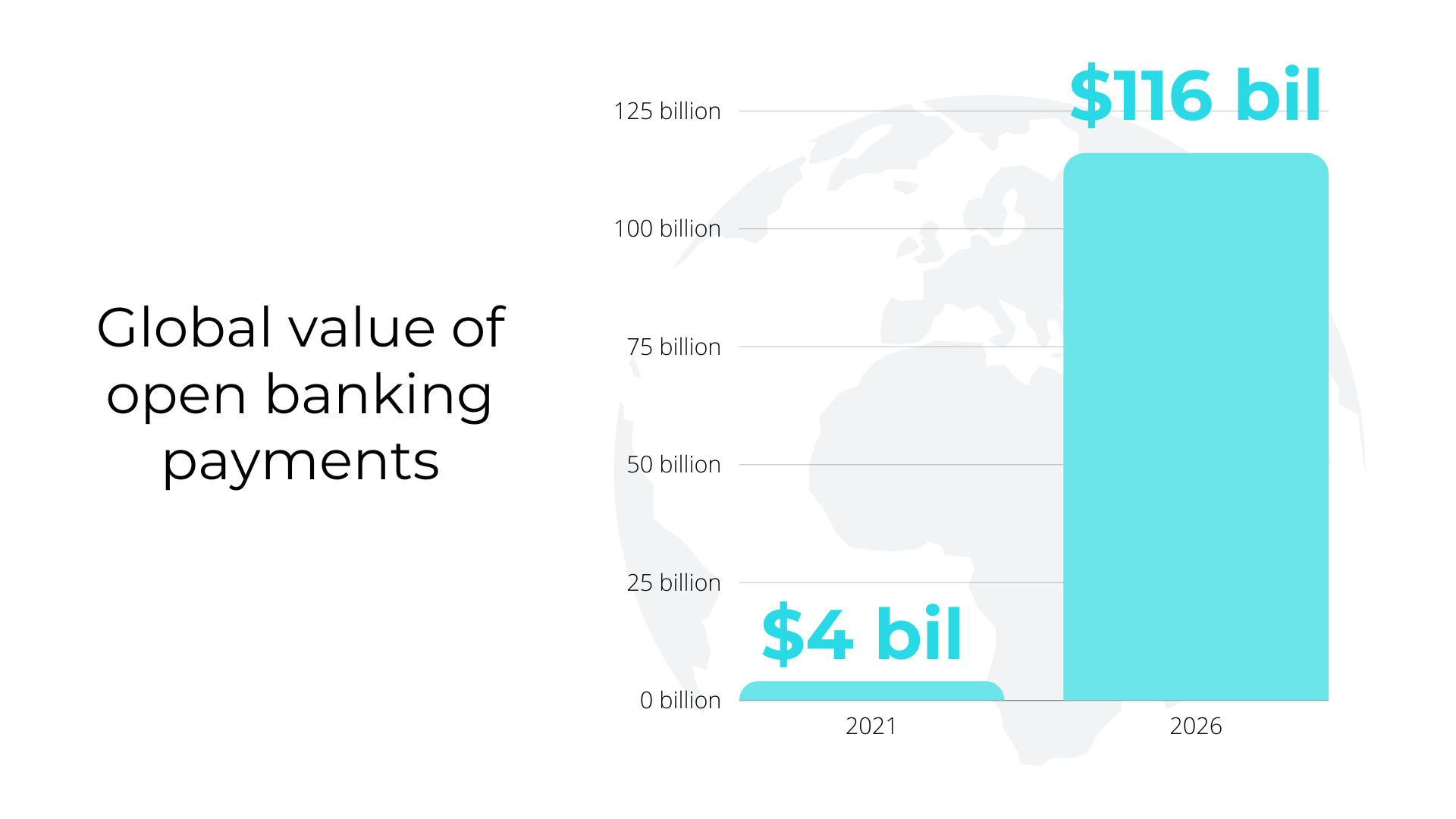

On its current growth trajectory, the UK surpassed 8 million monthly open banking payments by the end of 2022 and will reach 10 million by the end of the first half of 2023. The number of open banking users worldwide is expected to grow at an average annual rate of nearly 50% between 2020 and 2024. In terms of value, Juniper Research estimates the global value of open banking payments will exceed $116 billion by 2026, up from $4 billion in 2021.

When you think about open banking in the South African context, there are important insights to gain by studying open banking systems in other countries. This provides a guide to getting traction and learning from critical mistakes.

Regulatory frameworks differ depending on the jurisdiction. They may include rules for product and service offerings, data-sharing practices, permissions for third-party organizations to access data, and regulations regarding the reuse or redistribution of shared data. It is also important to consider legal issues such as obtaining customer consent for data usage and determining how banks are compensated for providing access. System implementation timelines also vary across countries but understanding these dynamics is essential when looking at open banking applications in Africa.

International regulatory frameworks

The revised Payment Services Directive (PSD2) in the European Union is focused on Opening Banking systems to third parties, assuming the customer gives their consent. This directive promotes data sharing and competition amongst businesses and encourages innovation. Through PSD2, banks can provide customers overviews of their various payment accounts as well as make payments via credit transfers on behalf of them.

Open banking is regulated by two organisations in the UK and Ireland. The Financial Conduct Authority (FCA) authorises companies to use open banking APIs for accessing financial data or initiating payments on behalf of a customer in the UK, while the Central Bank of Ireland regulates open banking in Ireland. It’s essential that businesses are authorised by these governing bodies before they can use open banking services.

In 2018, the Hong Kong Monetary Authority (HKMA) introduced the Open API Framework with the goal of making it easier for banks to use and access APIs. With Phase I of the Framework launching in January 2019, 20 banks are now offering more than 500 different APIs that provide customers with a wealth of information on banking products and services. The HKMA is continuing to work towards increasing API usage in banking. This governance framework is supervised monetary authorities. It’s also a collaborative and phased approach to implementing the API framework.

How the UK has succeeded in the Open Banking ecosystem

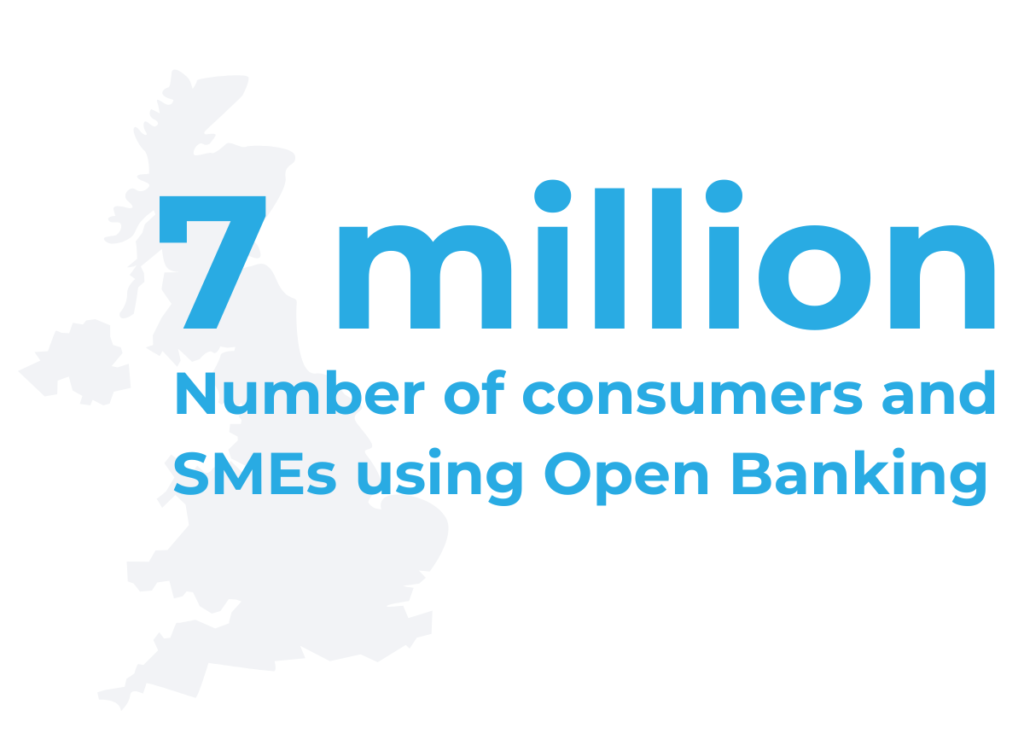

Open Banking LTD reports that seven million UK consumers and SMEs are now actively utilizing open banking services. Over the last year, we’ve seen the usage of open banking products and services in the UK change from basic account aggregation to innovative use cases, particularly in lending and identification.

For example, TrueLayer and Klarna offer Know-Your-Customer (KYC) products where customers simply allow access to their bank accounts to be verified for new product applications. The entire process only requires a small monetary payment to the relevant institution or banking partner. This eliminates time-consuming onboarding processes like filling out forms, lowering potential drop-off points in the process as well.

Neobanks such as Bunq are using open banking protocols to authenticate existing customers. This reduces call centre volumes and encourages customer loyalty by providing alternate solutions when card usage is blocked due to fraud or additional KYC requirements gotten up.

Fintern and Koyo are two online lenders who utilise bank account information to calculate an applicant’s creditworthiness quickly. Through bypassing traditional bureaus, no one’s credit score is affected during the procedure, making it convenient for those in search of financing without any risks.

How TrueLayer became a leader in Open Banking in the UK

TrueLayer is considered a trailblazer in the open banking landscape in the UK. The fintech company specializes in providing open banking APIs and infrastructure to facilitate secure and seamless data sharing between financial institutions, third-party providers, and end-users. Notably, they were among the first TPPs to successfully implement variable recurring payments (VRPs), introducing a paradigm shift in the industry. Their unwavering commitment to innovation is evident in their leading role in developing commercial VRP solutions for sweeping and non-sweeping use cases.

TrueLayer has developed a robust and reliable API platform that enables easy integration with financial institutions and seamless data exchange. Part of TrueLayer’s success has involved strategic partnerships with several UK banks, including Barclays, HSBC, and Lloyds Bank, among others. According to Forrester’s latest report, here’s why TrueLayer has come out on top:

- Distinguishing payments and consent capabilities: TrueLayer’s ability to address end-user issues through its “compelling” customer consent flow, which offers a customizable user experience by default.

- Developer-oriented approach: Their commitment to assisting clients in integrating open banking solutions. TrueLayer’s portal, comprehensive FAQs, and community guidance.

- Aggregated approach: By integrating with TrueLayer’s API, developers can retrieve account information, transaction data, and initiate payments across multiple banks and financial institutions, and the user only has to integrate into one system. This aggregated approach simplifies the integration process for developers and provides users with a unified interface to access their accounts from different banks.

- Impressive client track record and collaborative approach: The Fintech is known for being highly collaborative with the major UK banks and other fintech companies.

- Compliance and Security are number 1: they’ve had a strong emphasis on compliance with regulatory requirements, such as PSD2 (Revised Payment Services Directive) and GDPR (General Data Protection Regulation). They prioritize data security and employ robust security measures to protect users’ financial information during data sharing.

Are South African players ready to drive this revolution on the African continent?

South African banks have long been reputable and respectable institutions worldwide. Regulatory initiatives for open banking in South Africa are still absent and the country is lagging in terms of implementation. Restricted capabilities by South African banks result in the inability for 3rd parties to participate and add value to the financial sector. For South Africa to be a driving force in Africa, it will need to be more competitive to keep pace with the type of breakthroughs happening in countries like Nigeria.

The Central Bank of Nigeria has approved operational guidelines for open banking, marking the start of a new era for financial innovation and inclusion in Nigeria and Africa. The guidelines were released by the Director of the CBN’s Payments System Management Department on March 7, 2023. This development is the result of extensive collaboration between industry veterans, banks, fintechs, and international stakeholders. Nigeria has set an example for other African countries aspiring to develop their Open Banking ecosystems.

Who are the key players and what will their role be in implementing this ecosystem?

Regulators

The UK has the advantage of a regulated system, by the Financial Conduct Authority (FCA). However, in South Africa, only recently has there been a move towards regulating open banking. This can be viewed as a promising step forward. But, beyond simply regulating screen-scraping businesses, the South African Reserve Bank will need to broaden its scope to allow more momentum to develop by third-party fintechs.

The South African Reserve Bank (SARB) took a significant step on 23rd May by releasing a draft directive through its National Payment System Department (NPSD), specifically addressing the issuance of Instant Electronic Funds Transfer Credit (Instant EFT) payments. SARB will carefully consider all the raised points and subsequently issue the final directive, which will be legally binding.

This directive represents a noteworthy development in South Africa’s financial landscape, as it demonstrates a commitment to regulating and enhancing security. It responds to the growing demand from consumers for faster and more secure payment methods, as new payment innovations continue to gain traction in the market. This directive is a promising indication of the evolution of open banking. Beyond regulating open banking participants, the directive will need to extend the effort further to get all the banks to participate in a meaningful way.

Conversations around this ecosystem are picking up, and regulatory forums are being created like the Intergovernmental Fintech Working Group (IFWG) forum in 2016. IFWG consists of all the key players needed to drive open banking forward, being the financial sector regulators market conduct authorities, the competition authorities and industry players such as banks.

Financial institutions i.e., Banks

Financial institutions play an important role in securing data and providing customers with services and solutions to manage their finances. They act as the gatekeepers of data, safeguarding funds and offering tailored money management options. Open banking allows banks to access customer data and insights that may inform their decision-making. By implementing such a practice, banks can gain valuable insight into customer behaviour.

For example, Capitec Bank and Discovery Bank have seen major value in partnering with Easy Equities, where they have helped to create the biggest broker in South Africa. Beyond this, the partnership has provided significant value to Capitec and Discovery clients who now have an alternative method to save, directly in their banking app. Alternative banks like Bidvest Bank and Grinrod Bank have already partnered with fintech players such as Spot Money, Lesaka and Redcloud with business models that target a different section of the market such as SASSA beneficiaries in the case of Lesaka. Other banks who have dipped their toes in the water include, Nedbank and Investec, who are already making open APIs available. The biggest action and adoption will need to come from all the South African banks, not just a select few, as they are the ones that hold most of this data.

Investec

Investec is the only bank with API access made available to both consumers and businesses. The bank has made significant investments in the API platform space, starting with the Programmable Banking Community in collaboration with Offerzen. Initially focused on consumer data access, the platform has expanded to enable businesses to access consumer data with proper consent. Investec’s API continues to evolve with regular updates, and they maintain direct communication with the software development community through Offerzen’s Slack community. The API is lauded for its simplicity and straightforwardness, a rarity in the stringent security and compliance landscape of banking and finance.

Discovery

Discovery Bank’s app is geared towards an open banking landscape, where customers can easily access and create accounts for value-added products like Easy Equities. Customers are also able to improve their Money Status by integrating non-Discovery products e.g., retirement annuity, savings and insurance. The customer just must integrate or show proof of these products for the money status to improve. Whereas with FNB, if a client does not have an FNB product they will not be able to boost their eBucks level.

Capitec

Capitec Pay, which was built by Ozow, provides consumers with a fast and secure method of making online payments without the need to enter card or bank account details. With Capitec Pay, a customer can avoid sharing their banking information with online merchants. Instead, they can simply use their cellphone number and verify the payment through their banking app. This ensures a safe and secure online payment experience. The transaction will cost merchants R1 per transaction, which is a lot cheaper than other payment solutions.

Nedbank

In a noteworthy collaboration targeted towards SMEs, Nedbank partnered with Xero in 2021. This collaboration facilitates the seamless integration of banking transactions for small businesses. Specifically, it enables the automatic and secure import of transaction data from their Nedbank business accounts directly into the Xero cloud accounting platform. As a result, the need for manual data entry is significantly reduced, saving valuable time.

This integration empowers business clients to efficiently reconcile statements, generate intelligent and shareable reports, create online invoices, and access bank statements. Additionally, it provides them with the ability to review their cash flow in real-time from any location, enhancing convenience and flexibility.

Third-party providers (Fintech and SaaS)

As the catalysts behind open banking, third-party providers and fintech companies will greatly benefit from this new ecosystem because it gives them access to reliable financial data. They can use this to develop innovative financial products. It’s the role of these fintechs to build infrastructure in a scalable and secure way. These entities might not have the same resources or abilities as major institutions, however, the innovation and adaptability they offer will play a significant role in providing benefits to the banks.

There are several players in the Fintech space in South Africa that are pushing this evolution. Open finance platform truID allows users to securely access consumer financial data from all major banks in the country, with the aim of creating a unified open data framework. BankserveAfrica’s rapid payment programme, Payshap combines open banking APIs and instant payments which will help complete the process of payment request to settlement in a matter of seconds. EasyEquities, low-cost investment platform is one of the pioneers in open banking building partnerships with Capitec and Discovery to allow clients to buy and sell shares from within their banking apps. Ozow, a payment solution provider, has researched what consumers and businesses need, and has created a full suite of point-of-sale and online payment options. By collaborating with the major South Africa banks, they can analyse customer payment data using AI. Stitch is an infrastructure player in the market, which enables businesses to connect to the financial system and deliver payment experiences for their users. Recently they expanded their payments infrastructure offering by integrating Capitec Pay into its API.

Finch Technologies, a SaaS business offers on demand live quoting capabilities for business and consumer finance as well as open API infrastructure into affordability, verifications, and authentications.

Fears & challenges of Open Banking

Why is there reluctance to engage with Open Banking?

Security & potential data breaches

Open banking requires the sharing of data with third-party providers, which can, in the wrong hands, increase the risk of data breaches and compromise customer information. Banks may be hesitant to adopt open banking until they are confident that the technology is secure enough to protect customer data.

Global Lens: On the consumer front, 61% of North American customers are wary of sharing their data with a third party; whereas in the UK & Europe, only 53% are reluctant. The General Data Protection Regulation (GDPR) enacted by European governments has enforced a stricter adherence to privacy and data security, potentially leading to this favourable outlook on data sharing.

Beyond the customer roadblock, ensuring secure storage and transfer of shared information will be key for combatting cybercrime & money laundering. Stricter KYC checks should be adhered to in safeguarding customer assets and keeping their data safe from fraudsters.

Disruption

Another fear faced by financial institutions is that open banking may disrupt traditional banking business models. An example is where banks may have previously relied on their ability to control access to customer data in order to maintain a competitive advantage. There is now a bigger pressure than ever for consumers to have control over their data, as well as the many SaaS providers wanting to leverage the data.

Open banking presents an opportunity for banks to transform their business models and embrace new possibilities outside of their core level of expertise, especially if they move first. While there may be initial fears of disruption, banks can leverage open banking to their advantage and thrive in the evolving financial landscape.

By embracing open banking, banks can tap into a vast ecosystem of fintech companies and third-party providers. Instead of perceiving them as competitors, banks can view them as potential collaborators and partners. By forging strategic alliances and partnerships, banks can combine their strengths, such as trust, regulatory expertise, and established customer relationships, with the agility and innovation of fintech firms.

Cannibalisation of the customer base

In an open banking ecosystem, the concern of cannibalisation of the depositor base for banks is amplified because customers have more choices when it comes to banking services. Open banking allows third-party providers to access a bank’s customer data and offer their own financial services, which may compete with the bank’s own products. For example, a third-party provider could offer a high-interest savings account that competes with a bank’s own savings account. If the third-party provider can offer a better interest rate or more attractive features, the bank’s existing customers may be tempted to switch to the third-party provider’s account, which could result in the cannibalization of the bank’s deposit base. In this ecosystem, customers have greater visibility and transparency into the financial products and services available to them. This means they can easily compare and switch between products and providers, which can result in increased competition for banks. As a result, banks need to focus on offering competitive and innovative products to retain their customers and attract new ones. Additionally, banks need to be proactive in identifying customer needs and preferences and developing products and services that meet those needs. They also need to be aware of the competition and continuously evaluate and refine their offerings to remain competitive. By doing so, banks can maintain their deposit base and ensure their long-term viability in an increasingly competitive financial landscape.

What are the barriers and challenges for South African banks?

It is a next-generation technology that requires opening access to third-party institutions. SA banking has been well placed in its monopolistic market where it has not had to worry about opening access to other institutions for a long time. The biggest barrier right now is the mindset that this is possibly something that will consume the client base and revenue instead of enhancing it.

Here are a few other barriers and challenges that may slow down the advancement of open banking in South Africa:

Regulatory Challenges: All South African banks are subject to stringent regulations and compliance requirements imposed by regulatory bodies such as the South African Reserve Bank (SARB) and the Financial Sector Conduct Authority (FSCA). Adapting their existing systems and processes to comply with open banking regulations can be a complex and time-consuming task.

Legacy Systems and Infrastructure: Many traditional banks in South Africa have legacy systems that were not initially designed to interact with external third-party systems. Traditional banks infrastructure is often siloed for ‘credit’ ‘cheque’ ‘consumer’ ‘business’ etc. Each department is separate and, in some instances, so is the technology. Integrating these legacy systems with modern open banking APIs and technologies can be challenging and require significant investments in infrastructure upgrades, so SA banks will need to make big changes to their architecture to effectively pull it off.

Customer Trust and Education: Building trust among customers is crucial for the successful adoption of open banking in South Africa. Customers need reassurance that their financial data will be handled securely and with utmost privacy. The country’s history of data breaches and cybercrime incidents may contribute to customer scepticism. To overcome this barrier, South African banks must prioritize robust security measures and communicate them effectively to customers. Banks should invest in advanced encryption protocols, multi-factor authentication, and secure data storage practices. They should also comply with industry regulations, such as the Protection of Personal Information Act (POPIA), to ensure customer data is adequately protected. Transparent communication about these security measures, including providing clear explanations of how customer data is stored, accessed, and shared, can help alleviate concerns and foster trust. Additionally, educating customers about the safeguards of open banking is essential for its wider adoption and acceptance in South Africa. Banks can leverage digital platforms, including their websites, mobile apps, and social media channels, to disseminate educational content. Interactive tools, such as videos or simulations, can help customers understand how open banking works in practice and address any concerns they may have.

Digital access barriers: Innovation happens on the fringes, and this is also where alternative financiers tend to compete. These financiers cannot compete with banks on their cost of capital allocations; therefore, they tend to stay out of mainstream financial products. They innovate around the edges where they seek extra yield with alternative finance and insurance solutions. Although there is some benefit for previously excluded consumers with these alternative products, ultimately this data is not effectively used by banks to broaden the available product set offered by banks. Thus, financial access remains an issue for big groups of people. Banks, alternative financiers, and consumers all pay the price for this. Products remain unnecessarily expensive, banks miss out on new clients who are proving they can participate financially, and consumers fight to build a healthy banking portfolio.

So, while South Africa may have a high penetration of banked clients, there is room to argue that a large portion of these banked individuals and businesses are not receiving financial products and are thus financially excluded. In a recent Finch Technologies LinkedIn poll, we asked our audience what the biggest factors were contributing to South Africa’s digital payment challenges, and 53% of respondents said lack of education. This is still alarmingly true with 49% of consumers are still considered financially illiterate, and in addition to that 23.5% of South Africans remaining unbanked.

How does Open Banking benefit banks?

Banks are nervous about loss of income and clients, but the upside opportunity is the vast array of additional (traditional non-bank products) services that could be provided by banks to their clients. In essence, opting for an open banking ecosystem and leveraging a SaaS business offering, increases the banks current value proposition. Here’s a look at some of the main benefits of embracing an open banking ecosystem:

Collaborative and Innovative Advantage

Open banking gives an opportunity for banks to stay ahead of the competition by letting them explore data-sharing agreements with third-party providers and other non-financial service institutions.

There is an opportunity for banks to use open banking to allow innovators to create products around the banking ecosystem that service the bank’s clients in an efficient manner. The opportunity for banks is to work closely with the innovators and mavericks to create tools, products, and functions that benefit the banks’ clients.

Theoretically, this creates an enriched customer database and more revenue opportunities. Looping this data back into the banking ecosystem enriches the dataset available to score clients who are looking for mainstream products.

It can often be difficult for non-banks to compete in core banking products primarily due to the cost of capital. An ideal example is Bayport, which is one of South Africa’s largest personal lenders. Although it is well established and provides a great service, it has a cost of capital that is higher than retail banks. This has limited its scale and ability to push on and become a significant player in the personal lending space, which is still massively dominated by large banks.

Rather than investing time and resources in building niche products, it is more beneficial for large retailers or corporate banks to actively observe innovators and their directions. By doing so, banks can identify the winning trends and segments that would benefit from becoming part of their mainstream offerings. This approach allows banks to leverage the expertise and innovations of external players, enabling them to stay competitive. Using the knowledge from these external players, they’ll be able to establish a strong development pipeline or acquisition pipeline, ensuring they offer relevant and impactful solutions to their customers.

Better customer engagement & forecasting

Open banking APIs offer the potential to radically transform the way banks interact with customers. By using open-source technology to merge banking and fintech institutions, customers are offered an innovative, holistic service that meets all their changing needs. Banks now have the chance to more deeply engage with customers and foster relationships of trust by providing user-friendly customer experiences revolving around aggregated, accessible financial information. An improved interface can help create a less intimidating space for customers and encourage them to be in better control of their finances. Banks, as we know, can then gain insights into a customer’s habits and preferences for offering tailored communication and services that meet their exact specifications.

Financial institutions will be able to identify and adapt to evolving data privacy standards, enabling them to gain insight into the future of customer experience. The ones who successfully embrace this ecosystem will be able to utilize data to inform decision-making and shape strategy, discover new customers and effectively cross-sell existing products and services. This ideal picture means that banks can create customised experiences, while also bolstering retention rates, and earning market share. This ecosystem presents an incredible opportunity to not only drive customer loyalty and engagement but also increase the bank’s revenue stream.

Simplified compliance & reduced costs

Open banking holds the promise of easing compliance burdens and lowering costs. This ecosystem relies on standardized APIs to facilitate data sharing between financial institutions and third-party providers. This makes it easier to manage and exchange data, streamlining processes, minimizing complexity and associated costs. By utilizing these APIs, banks can reduce the amount of manual labour needed for operations while achieving an efficient flow of information across different organizations. Additionally, new KYC and Anti-Money Laundering (AML) protocols can potentially be developed from the ability to access data across different platforms. Traditional banks routinely keep track of consumer data, yet prevalent KYC/AML costs are anticipated to be shared among service providers who have access to said data.

Embedded finance

Embedded finance provides a huge opportunity for banks, where non-traditional industries are starting to offer financial products and services that used to be provided by banks. Open banking can facilitate the data sharing and connectivity required for embedded finance. An ideal example is a large retailer that starts to offer credit cards in partnership with a bank, or as part of their own offering. With open banking, there is greater opportunity for banks to participate and benefit by e.g., sharing their data, than for them to be excluded and be seen as competitors only.

Being open to embedded finance from alternative providers allows banks to access an entirely new customer base that they may not have been able to reach otherwise. Very typically those who are referred to as “unbanked”. This will also be a huge cost saving as often the retailer and Fintech provider will take on all the costs when building out the product. Additionally, these Fintech providers aim to build seamless and user-friendly experiences, with the focus on ensuring customer retention. Consumers want integrated financial solutions, and they need to be as accessible as possible.

Re-package financial products

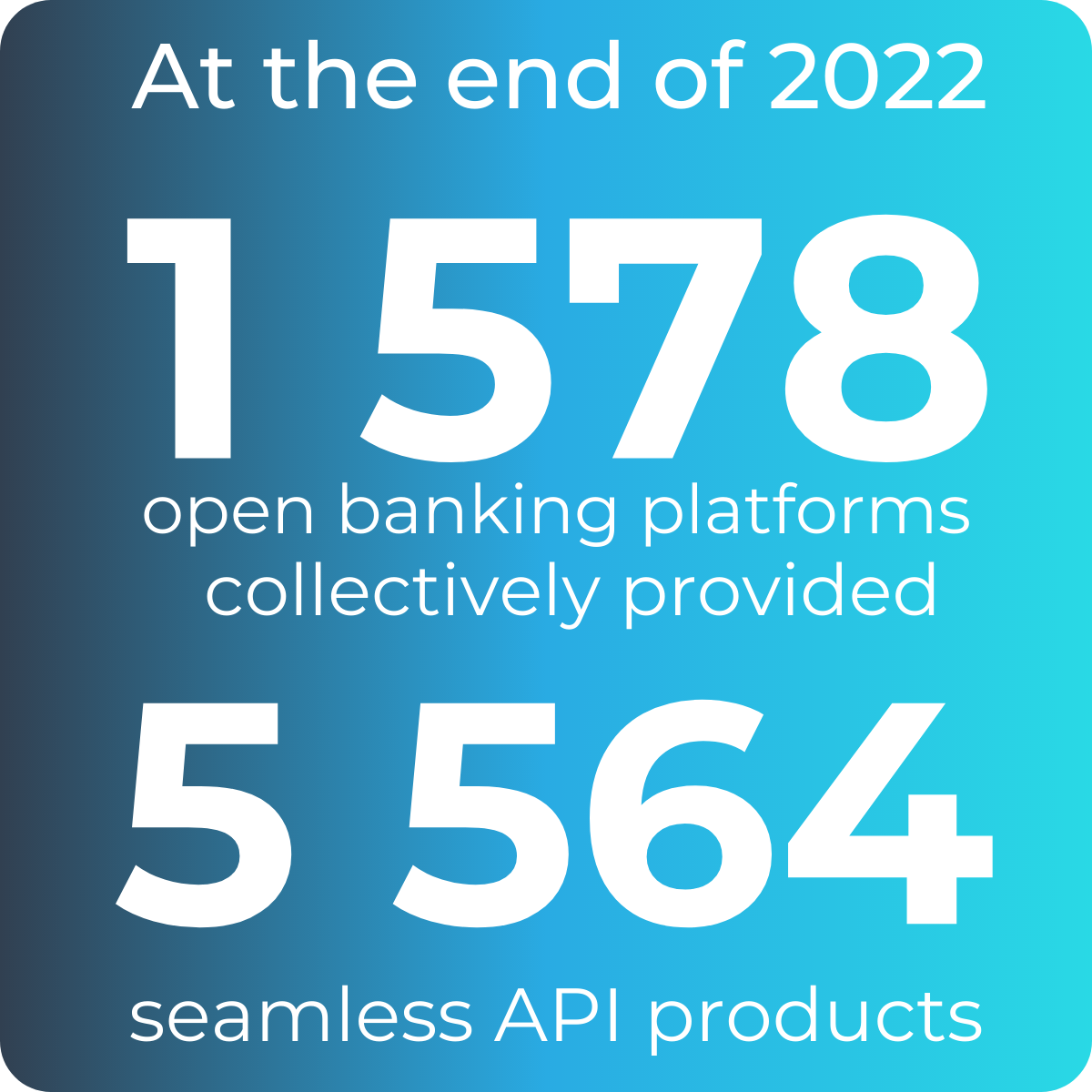

As the fintech sector continues to grow, customers are presented with more choice in terms of banking products and services. This leads to customers no longer being tied to traditional bank packages and instead opting for tailored services from both fintechs and banks. As a result, it is becoming increasingly popular for banks to unbundle their existing financial offerings and contract out specialized parts of their products. Open banking offers banks the opportunity to unbundle large banking services into smaller components which can then be re-bundled in a customer-focused manner. In essence, they can shed off less profitable parts of their product bundles, and re-package them with the assistance of fintechs. One such example is TymeBank’s product called GoalSave. This feature allows customers to create savings goals and allocate funds towards achieving them. By re-packaging traditional savings accounts into goal-oriented products, TymeBank enables customers to track their progress and save effectively towards specific targets. At the end of the second quarter of 2022, there were 1,578 operational open banking platforms. These platforms collectively provided a comprehensive range of 5,564 API products.

What does Open Banking look like in South Africa?

South Africa is a country that could benefit massively from a well-developed open banking market. There are over 600 insurers and 6000 lenders that could all form part of the open banking environment. Each quarter there are over 30 000 000 applications for loans, insurance products (account information) and mobile contracts. Resulting in over 3000 products that require recurring payments. South Africa has the benefit of one of the most established banking technology and platforms. The next iteration is making it work for a broader market. Here are a couple of case studies of companies and sectors that are doing it right so far in South Africa:

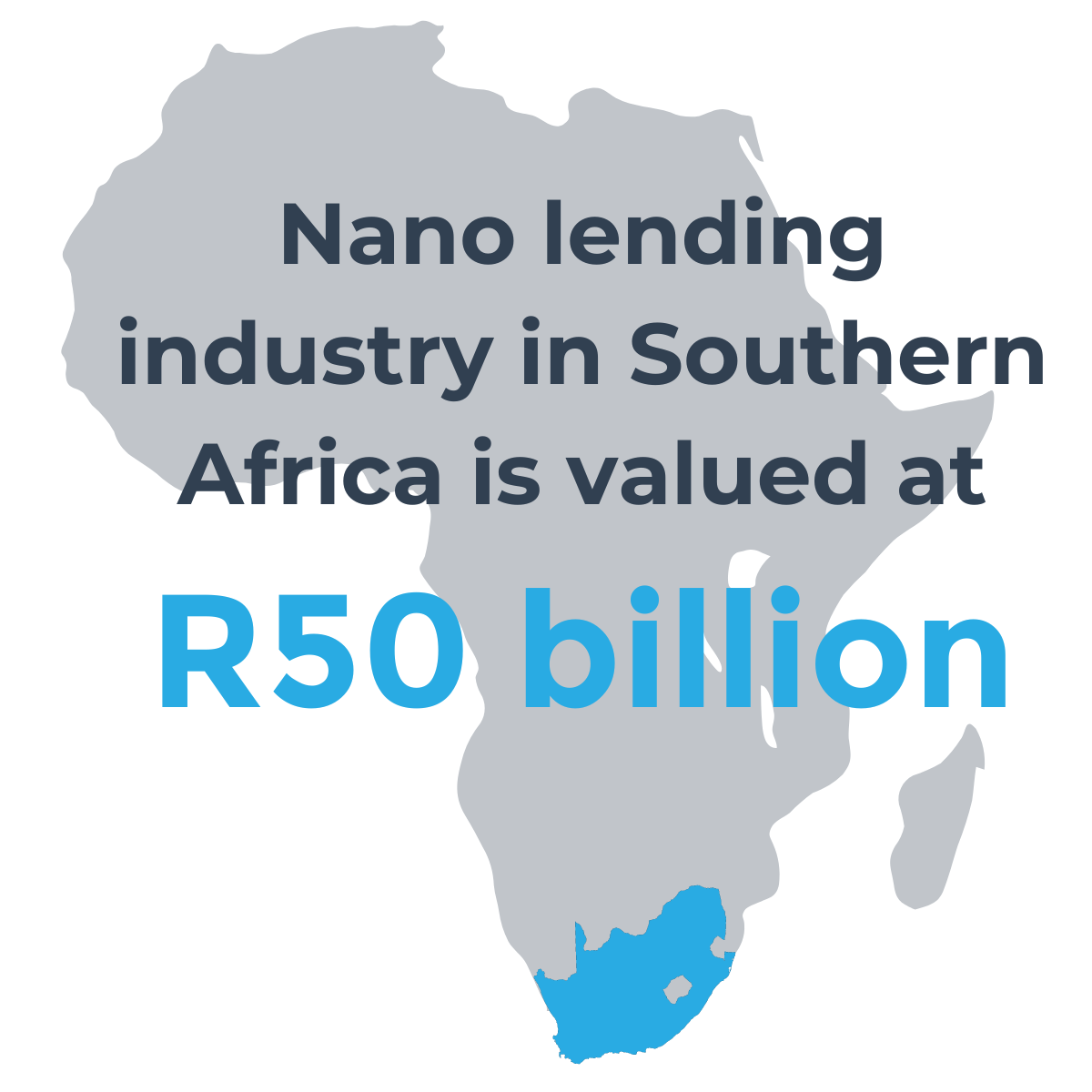

Nano Lending

Looking at small Airtime Advances gaining traction in the market, a large mobile operator wanted to enter into the lending space through a product concept called Nano Lending. This is typically an advance of R50-R1,000 paid back anywhere from 7 days through to 21 days.

Due to the nano size of the loan, there could not be any human intervention in the scoring process. Gathr, a prime example of a Fintech developing open banking ready software, was used for the digital onboarding solution required. The mobile operator was able to acquire all the financial transactions which included main income, debit orders and all expenses to conduct an affordability assessment. All this information is passed into a risk scorecard and from application to approval is done in minutes.

Taxi Finance

South Africa, like most Sub-Saharan African countries has a booming minibus taxi industry. There is a significant amount of physical cash that is traded in this space. This includes the taxi operators paying off their vehicle finance in weekly instalments with cash.

A leading South African taxi finance business is looking to digitise its collections. Their preference for these collections is linked to the extra cash handling costs, risk of violence and theft around cash and the added difficulty of cash reconciliation.

This business is looking to use an open banking solution to calculate the seasonality of a taxi owner’s cashflow to calculate optimal strike times in a month to collect the capital and interest owed on a loan. By digitizing these transactions, one is quickly able to build several forecasting models using seasonality analysis.

Through this process, the taxi owner has the added benefit of not having to deliver cash, has efficient seasonality analysis to optimise collections to avoid failed collections and access to a product that is not a mainstream product of a bank.

Merchant Services and Payments

Open banking has revolutionized merchant services and payments in South Africa. Fintech companies leverage open banking to build payment solutions that allow merchants to accept payments directly from customers’ bank accounts, eliminating the need for card-based transactions.

A notable illustration of this symbiotic relationship between banking and fintech can be witnessed within the South African payment solution provider space. By integrating with all major banks in the country, Ozow, a payment solution provider, has recently joined forces with a prominent bank, Capitec, to successfully introduce Capitec Pay, the country’s pioneering payments API.

Additionally, payment system provider BankServeAfrica launched PayShap, a Payment Initiation Service App (PIS). Combining PIS apps with open banking APIs and instant payments can revolutionize the payment process, enabling seamless transactions from initiation to settlement within seconds. By utilising PIS apps, retailers accepting payments can ensure prompt payment settlement before releasing goods to customers.

While banks will continue to receive payment initiation requests, their role remains crucial as they are responsible for facilitating instant payments. To retain retailers as customers who rely on instant settlement, banks need to ensure optimal performance of their payment’s platforms.

Although in the early stages there are significant prospects for banks willing to embrace the transformative potential of instant payments.

Personal Finance Management

Personal finance management tools are poised to become the flagship sector of open banking, empowering individuals to take control of their financial lives by seamlessly accessing and managing their accounts. PFM applications are expected to reach a global market value of $3.3 billion in 2025, which is a CAGR of 12.65% from 2018.

Open banking APIs have empowered financial institutions and fintechs to develop personal finance management (PFM) applications. These apps aggregate data from multiple bank accounts, credit cards, and other financial accounts, providing users with a comprehensive view of their finances in one place. Users can track their expenses, set budgets, and receive personalized financial insights. Open banking ensures that the data is securely accessed and updated in real-time, enabling users to make informed financial decisions. Discovery Bank has done this with Vitality Money, where consumers can track their financial behaviours and improve their status.

Does open banking augment or challenge how banks make their money?

Traditionally, banks have been set up to make money on consumers’ deposits and lending activities. How does that work? A basic example of this relationship is when a consumer deposits their money into a bank account to keep it safe and accessible. If a consumer chooses to put their money in a long-term savings account, they can earn interest on it. Banks then utilise these funds to provide loans to businesses and individuals at an interest rate higher than what they pay to the consumer. This interest differential, considers factors like default rates, is how banks aim to generate profits. While banks have developed more sophisticated models, this simplified explanation highlights their traditional revenue approach.

A big shift in banking has been towards the fees that banks earn from their clients. For example, Capitec has evolved as a bank where a large portion of its earnings were interest income compared to now where more than a third of its income comes from fees. In essence banks make money from lending your money at a greater rate and by charging fees. So, why should there be any reluctance to embrace the open banking landscape? This model at its core is all about opening up the ecosystem to other providers. Banks are worried that opening their data and their payment rails will lead to a flurry of lenders and wallet providers that may eat into their deposit base and their lending base. If anything, it allows banks to bring in revenue through direct streams, where previously they relied on global payment processing networks e.g., Visa, now they can cut out the middleman and improve profitability. Open banking will sit alongside traditional revenue streams, where various fintech tools will assist in efficiencies and customer retention.

Repackaging products and creating additional product offerings based on open banking data, will allow banks to create an even larger revenue pool, where consumers can now take out additional insurance offerings or make use of financial health tools all within their banking ecosystem. Customer retention will be a key focus for banks going forward, mainly as customers will be looking for the best service provider coupled with the cheapest banking fees, and it’s cheaper for banks to keep a client than it is to bring in a new one. open banking infrastructure will allow banks to offer consumer’s the diverse services they need at a reduced cost.

What is the way forward for open banking, and which direction are the players leaning?

Open banking in South Africa hinges on active collaboration between regulators, banks, and stakeholders to foster financial inclusion, drive innovation, and unlock new unlock new opportunities for banks to deliver value.

Open Banking is rapidly becoming part of the narrative in the traditional banking landscape. To stay competitive, many established banks are now realizing they must have an Open Banking strategy. It can be difficult to monetize APIs beyond account aggregation; however, incentives for customers could be extremely helpful in capitalising on Open Banking opportunities. These benefits may include faster loan applications and reduced credit score impact, simplified KYC processes or credential requirement simplification, and leveraging existing fintech innovations rather than starting from scratch.

In South Africa, some banks are embracing these changes while others remain against them—regardless, incumbents and neobanks will be able to leverage Open Banking to their advantage by providing attractive customer incentives. This underscores the importance for traditional banks to embrace this ecosystem and avoid falling behind their more progressive counterparts.

Conclusion

While South African banks have initially approached open banking with caution, there are significant benefits and market opportunities to be gained by embracing this landscape. Key players in this ecosystem will need to take it one step further than just being idealists, they will need to help both create and embrace Open Banking regulatory frameworks and groups.

Global players have demonstrated the success of open banking, and market projections forecast significant growth in the next five years. To stay ahead and remain competitive, it is essential for South African banks to embrace open banking and leverage its potential for customer-centric solutions and securing a prominent position in the evolving financial landscape. This is an opportunity to combat financial exclusion, collaboration between Fintechs and banks is crucial in developing accessible and affordable financial products for South Africans.

Participating banks have a significant opportunity to gain a competitive edge within the Open Banking landscape. Those banks that seize the initiative and make the initial move will enjoy a compounded advantage in the market. Catching up with these pioneering institutions will prove challenging, given the increasing elasticity of customer behaviour.

Further reading:

Open banking benefits for customers, businesses, and banks – GoCardLess

Report on Intergovernmental Fintech Working Group – Financial Intelligence Agency

The Main Challenges of Open Banking – Penser

Open Banking explained: everything you need to know – Kevin

The Future Of Financial Services: Developing Your Open Banking Strategy – Forbes

The future of open banking and why banks should take the lead – Monroe

5 Benefits of Open Banking for Banks – Tarabut Gateway

How Financial Institutions Can Benefit From Open Banking? – Zuci Systems